Impact bonds are on the cusp of a turning point. With a 34% share of the 502 billion USD impact investing assets under management by the end of 2018, private debt is the largest asset class in impact investing. It has therefore shifted from an investment debated solely by a handful of do-good forerunners to a hot topic that professionals from larger financial institutions are now eyeing and are no longer afraid to ask about at dinner parties.

At Symbiotics, we have been in the impact investing business in frontier markets for over 15 years and we are glad that a growing number of pension funds, insurance groups, global banks and large asset managers across the globe are embracing this asset class. Here are some answers to the most common questions we’ve been asked about impact bonds.

Question 1

“Does impact investing through private debt really earn solid returns?”

The impact bond story is not a story of speculation and volatility. It is the real-life story of opening of financial services to millions of unbanked households and micro-entrepreneurs who need working capital in emerging and frontier markets, some of the fastest-growing in the world.

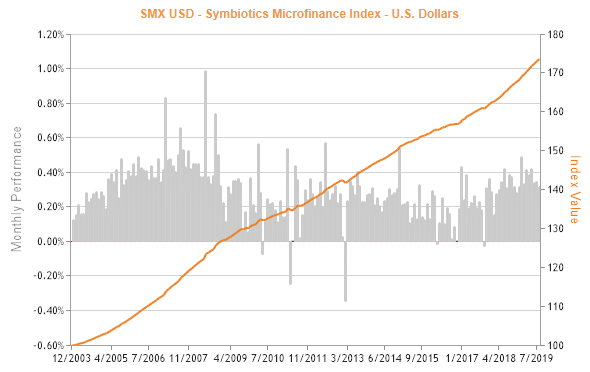

By investing in such markets, portfolios containing impact bonds directly benefit from the 5-6% annual economic growth and 3-4% population rates prevailing there, attractive interest rates and unsaturated credit markets. And impact bonds’ track record supports this - see Chart below. In 2018, the SMX (i.e. the Symbiotics Microfinance Index, aggregating and tracking the main global fixed income funds that target microfinance institutions in developing countries) posted a return of 3.88%, with a lower volatility than other asset classes (0.56% from 2003-2019, compared to global bonds’ 2.99%, for instance).

By virtue of their differing risk profile from traditional bonds, they can act as a great portfolio diversifier, while also providing a through-road into local currencies to hedge against dollar-denominated assets. So, in answer to the question, yes, you can earn a solid return from impact bonds.

Impact bonds. Stable and steady returns since 2003

Question 2

“How risky is the business of lending to the unbanked?”

Though enticed by the idea of contributing to resolving some of the world’s wicked problems or, say, promoting social and economic inclusion, some investors might be turned off by the risk associated with these low-income end customers’ limited ability to repay their loans. Yet, statistics show that the vast majority our microfinance loan recipients repay their loans and interest in full, meaning the risk profile of impact bonds is not tainted by the “poverty” of their beneficiaries.

A recent survey of 63 microfinance investment funds showed that in 2017 the ratio of loans written off was 0.3%, down from 0.5% the previous year. What’s more, the average credit loss rate among all of Moody’s rated issuers fell to 0.7% in 2017 from 1.5% the previous year, and historically, the annual credit average loss rate has been 0.9% since 1983.

Just to be pragmatic, you could compare that to the 2.59% for mortgages or 2.56% for credit cards in the United States, but you get the picture: impact bond funds can offer high portfolio quality.

Question 3

“How do impact bonds differ from mainstream finance products?”

Impact bonds try to address a range of global challenges, which are being addressed by the United Nations 2030 Agenda for Sustainable Development and its associated Sustainable Development Goals, including no poverty, zero hunger, good health and well-being, quality education, gender equality, clean water and sanitation, affordable and clean energy, decent work and economic growth.

Along with other development finance investments, impact bonds stand out from mainstream investments because they pursue a “double bottom-line” promise that is implemented through upstream-stated intent and downstream measurement centered either on social or environmental objectives. These typically include (1) pre-investment ratings, (2) transactional covenants binding the use of funds to the targeted goals, and (3) post-investment reporting, on (a) the investment output produced, on (b) the investment outreach achieved in terms of breadth and depth into bottom of the pyramid population, and in some cases (c) on the ex-post outcome results delivered, attached to their specific stated-intent.

Question 4

“If impact bonds are so attractive, why aren’t more banks and investment providers jumping on board to sell them?”

While many larger banks are now waking up to the reality of fast-growing demand for and benefits of impact investing and impact bonds, the barrier to entry remains high. Properly building, selecting or managing impact bonds within portfolios requires not just human capital but commitment. Regulations are stringent; set-up costs are high. Many banks simply lack the depth of impact expertise or the required expertise and presence in emerging markets. As a result, despite rising client demand for impact products, most banks simply do not have the bandwidth to deliver a compelling offering. For example, Barclays reported that more than half of its clients are interested in investing in impact, but that only 15% of its clients actually had done so in 2017. This suggests a wide gap between demand and the banking sectors’ ability to meet it. This is why it makes sense for institutions to partner with an expert that already has the expertise and the connections on the ground to deliver impact through the most efficient channels.

Question 5

“What expertise is necessary to maximize the financial and socioeconomic returns of impact bonds?”

Since 2004, Symbiotics has built the know-how and broad network of local partners, which have allowed us to develop our impact debt origination expertise. A bit like a Michelin-starred chef knows where to source the best produce to deliver the best recipes, we have learned how to select our local partners carefully to ensure their practices are protective of the end beneficiaries of the microfinance loans.

This involves rigorous scrutiny and close monitoring of each deal, with an eye for the bottom line. For that, we use a rich set of qualitative and quantitative indicators, analyzing credit risk along eight dimensions, including financial performance, business model and governance. We conduct face-to-face interviews with several staff at each of our potential “investees”, to perform a comprehensive due diligence, and regularly conduct checks of some 100 business health indicators at 272 local microfinance institutions in 72 countries. We also monitor documentation, covenants and ensure timely payment collection.

To ensure maximum socioeconomic returns on impact bond investments also requires doing a lot of homework. Though most of the institutions we consider have endorsed the Smart Campaign Client Protection Principles and quite a few are in the process of being certified, at Symbiotics we also review them during a thorough due diligence process to make sure borrowers are not over-indebted. We systematically perform a social performance assessment of our partners, which includes reviewing their lending practices. In addition, our annual know-your-customer (KYC) checks on institutions include reviewing any press coverage of their business that might mention aggressive lending practices for instance. Lastly, we meet with representatives from the local Microfinance Association whenever possible to get a third-party opinion about the institutions’ reputation and practices. In short, we are constantly working on improving these measures to ensure that we offer the best company profiles to our clients, while being mindful of the livelihood of the borrowers that constitutes our impact promise, and measuring effective results against it.